Table of Contents

Title: The R100 ‘Easy Credit’ Trap: How ‘Buy Now, Pay Later’ is Draining Your R390 SASSA Grant in 2026

It’s March 2026, and let’s be honest—trying to make ends meet in South Africa right now feels like a losing battle. Everywhere you look, ‘Buy Now, Pay Later’ (BNPL) offers are popping up like mushrooms after rain. They promise a helping hand, but for anyone living on a R390 SASSA grant, these deals are often a disguised trap. I’ve looked into how a simple R300 purchase can quickly morph into a R500 debt nightmare. We need to talk about the tactics these companies use and how you can keep your grant money where it belongs: in your pocket.

{kind=link}

The Rise of the ‘Easy Credit’ Promise: What is BNPL and Why is it Everywhere in 2026?

The BNPL model is the biggest trend hitting South African shops in 2026, and quite frankly, it’s a massive threat to your R390 SASSA grant. You’ve seen the names—PayJustNow, Afterpay, and Payflex. They let you walk out of Pick n Pay, Bash, or Cape Union Mart with your bags full while only paying a fraction of the cost upfront. When you’re staring at a tight R390 budget, splitting a R400 bill into four R100 payments feels like a miracle.

The FSCA reported in March 2026 that these transactions have shot up by 200%. Most of that growth is in small purchases under R1000, which is the exact price range for most social grant recipients. The system is built to be “frictionless,” which is just a fancy way of saying they make it too easy to say yes. Unlike a traditional lay-by where you wait for your goods, BNPL gives you that instant hit. It makes you forget that you’re signing away money you don’t even have yet. If you’re trying to time your shopping with your next payout, check our Payment Dates page, but please, be careful with these “easy” offers.

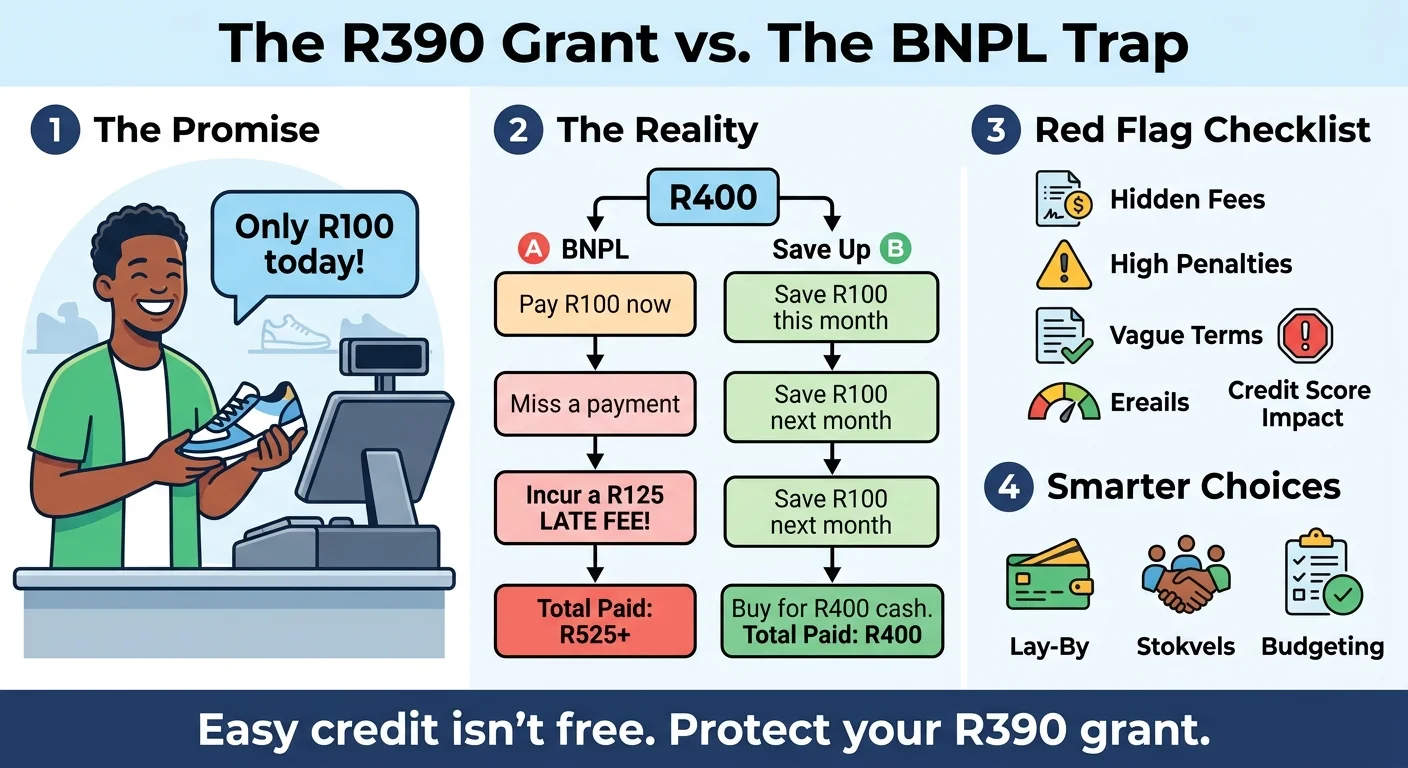

Investigation: How a R300 Pair of School Shoes Becomes a R475 Debt Nightmare

Let’s look at how this trap actually snaps shut. Say your child needs school shoes for R300. You’ve got R150 left from your grant after buying maize and oil. The cashier says you can take the shoes today for just R75. You figure you’ll pay the rest over the next few weeks. It sounds like a win.

But life happens. Maybe the taxi fare goes up or someone gets sick. Suddenly, your bank account is empty on the day the third payment is due. That BNPL provider doesn’t care about your emergency; they’ll slap you with a R125 late fee immediately. Now you don’t owe R150, you owe R275. Throw in a monthly service fee, and those R300 shoes have cost you nearly R500. Data from the National Credit Regulator shows that 40% of users missed a payment in 2026. For a SASSA beneficiary, that R125 fee is a week’s worth of food. It’s a debt spiral that’s incredibly hard to climb out of.

The Psychological Trap: Are Retailers Exploiting Vulnerable Consumers?

I’ve spent time analyzing these checkouts, and I’m convinced this isn’t an accident. It’s a calculated move to target people who are struggling. When a shop says “4 easy payments,” they are tricking your brain into thinking the item is cheaper than it is. It removes the pain of paying.

Dr. Thandiwe Ngcobo from Wits put it perfectly in a recent interview: it gives a temporary sense of relief but just delays the suffering. To me, this feels predatory. We’re talking about people on the R390 grant who are already vulnerable. It’s essentially reckless lending hidden in a legal loophole. If you feel like you’ve been played, you don’t have to just take it. Our Appeals Guide shows you how to fight back and formalize a complaint, which you can use for consumer issues too.

Red Flags: Your Checklist to Spot a Dangerous BNPL Deal Before You Click ‘Accept’

You have to be your own bodyguard when it comes to your money. Here is what I look for to spot a bad deal in 2026:

- Crazy Late Fees: Check the fine print first. If the penalty is more than 20% of what you owe (like a R100 fee on a R200 bill), run away.

- Hidden Terms: If the contract is ten pages of legal jargon, they’re hiding something. You want clear, simple rules you can understand.

- Credit Score Damage: Some of these guys report you to credit bureaus. One missed R100 payment could stop you from getting a house or a proper loan years from now.

- No Humans to Talk To: If you can’t call a real person when things go wrong, don’t trust them. Chatbots won’t help when you’re broke and need an extension.

- The ‘Spend More’ Push: If the app keeps telling you to increase your limit after one successful purchase, they want you trapped in debt.

Smarter Alternatives: How to Get What You Need Without Falling Into the Debt Trap

That “buy now” rush is addictive, but nothing beats the peace of mind of being debt-free. Your R390 grant is for survival, not for paying off some tech company’s interest. Here are better ways to handle your money:

- Go Back to Lay-By: It’s the safest way to shop. No interest, no fees, no stress. You get the item when you’ve actually paid for it.

- The Power of the Stokvel: We wrote about the ‘R390 Stokvel Revolution’ for a reason. When five friends put in R200, you have R1000 cash. No credit needed.

- Build a ‘Sinking Fund’: It’s just a fancy name for a savings jar. Put away R50 a month in a no-fee account like the Khulisa Account. It feels amazing to buy something with your own saved cash.

- Swap and Shop Second-Hand: Use WhatsApp groups or Facebook Marketplace. Kids grow out of stuff so fast. Buying used items keeps your grant money in your pocket and is better for the planet too.

Frequently Asked Questions

Can I use my SASSA grant to sign up for Buy Now, Pay Later services in 2026?

What happens if I miss a BNPL payment while on the R390 grant?

Are BNPL services like PayJustNow regulated in South Africa in 2026?

Is using BNPL better than taking a loan from a mashonisa (loan shark)?

How can I check if a BNPL purchase will affect my credit score in 2026?

Where can I get help if I'm already in debt from BNPL services?

Read Next

SASSA Easter Payout CONFIRMED: Get Your R390 April Grant Early for the 2026 Holiday Weekend

BREAKING NEWS for March 2026: SASSA has officially confirmed that April 2026 …

SASSA's R10 'Khulisa Account': Your Guide to the New Low-Cost Bank Account for 2026

BREAKING March 2026: The South African Reserve Bank has mandated a new …

Comments & Discussions