Table of Contents

Title: The R100 ‘Easy Payment’ Trap: How Digital Loans & BNPL Are Draining Your R390 SASSA Grant in 2026

I’ve been watching a worrying trend lately where a simple R100 purchase ends up eating a person’s entire SASSA R390 grant. This investigative report for April 2026 looks at how Buy Now, Pay Later (BNPL) and instant digital loans are aggressively targeting grant recipients in South Africa. We’re looking at the hidden costs, the soul-crushing debt cycles, and a real plan to protect your money from these digital predators.

{kind=link}

The New Digital Predator: How a R100 T-Shirt Becomes a R390 Grant Nightmare

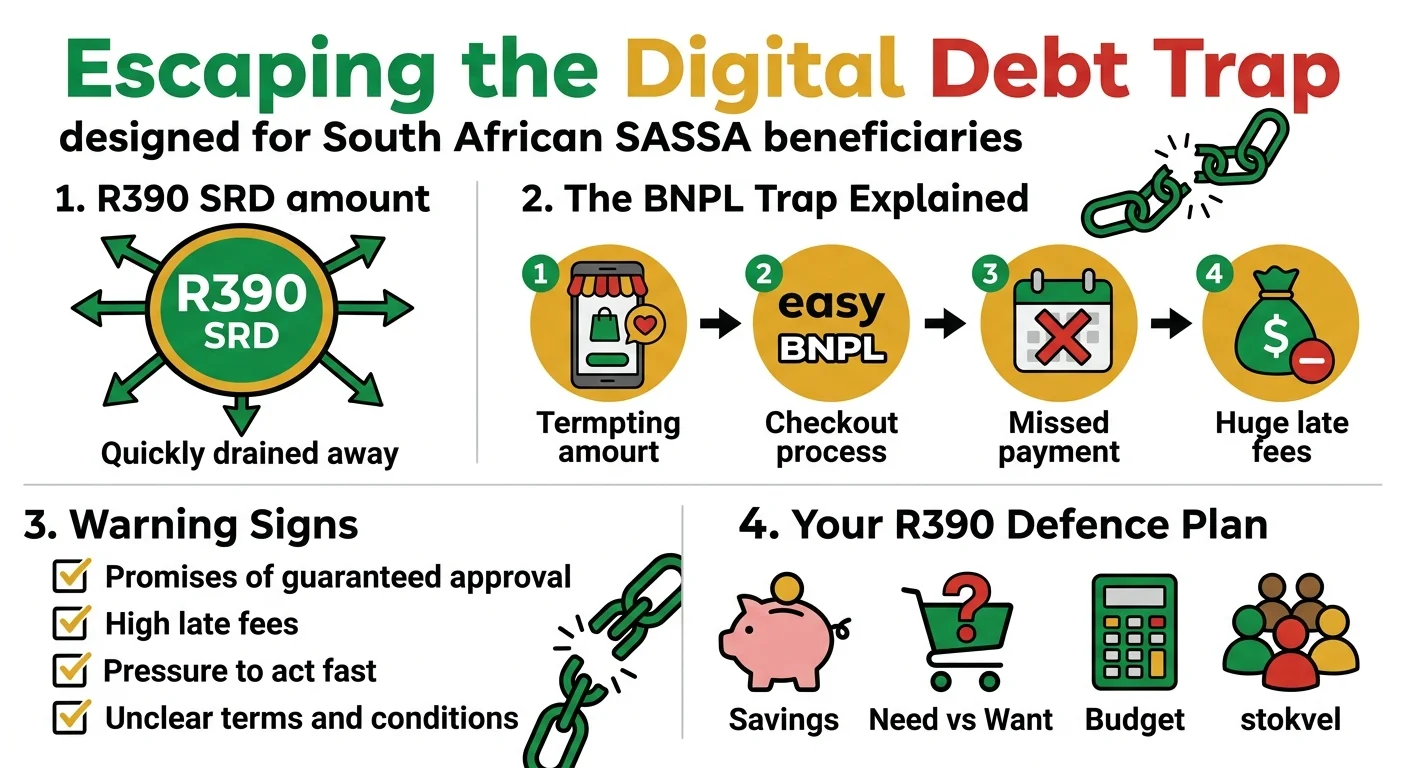

The loan sharks of 2026 don’t hang out on street corners anymore. They live right inside your smartphone, hiding behind the “convenience” of a shopping app. These services, known as ‘Buy Now, Pay Later’ (BNPL), are the biggest threat I see facing SASSA beneficiaries today. They turn a small R100 buy into a debt spiral that swallows a R390 grant before you even see the cash.

A report from the Consumer Justice Foundation in April 2026 shows that 35% of SRD grant recipients have used a BNPL service, and they are failing to pay back these loans three times more often than people with regular salaries. These apps promise speed and ease, appearing like a lifeline when your grant is running low. They offer to split a small cost—like airtime or groceries—into “three easy payments.” It sounds helpful, but it’s a trap. These companies actually count on you missing a payment. That’s when the “free” service hits you with massive late fees and account charges. For someone living on a R390 grant, an R80 late fee is a disaster. That is 20% of your monthly income gone in a second.

Unpacking the Deception: The Hidden Costs and Psychological Tricks of BNPL Apps

What worries me most is how these apps play mind games with people. They are experts at making things you can’t afford look cheap by breaking down the price. Financial psychologist Dr. Aisha Ndlovu says our brains see four payments of R50 much differently than one payment of R200. The smaller number feels safe, so we stop worrying about the total cost. This is a deliberate tactic to get you to spend.

Here is how the trap actually works:

- The ‘Interest-Free’ Lie: They promise no interest, which is how they get you through the door. But their whole business relies on penalties. One missed payment triggers a late fee of R80 to R150. When you look at the math, these penalties on a small purchase can be the same as paying 1000% interest.

- Too Easy to Buy: BNPL buttons are everywhere now, from online checkouts to shop counters. It’s so fast that you don’t have time to stop and think if you actually have the money.

- They Take Your Money First: When you sign up, you give them permission to take money from your bank account. The moment your SASSA grant hits, they grab their share first. It doesn’t matter if you need that money for food or a taxi. Data from the National Credit Regulator (NCR) shows a 250% jump in complaints about these digital debits this year.

Why SASSA Beneficiaries Are the Primary Target in 2026

It makes me angry to see how specifically these lenders target the most vulnerable. They love SASSA beneficiaries because the income is guaranteed by the government. They know exactly when the money arrives. I’ve noticed that ads for these loan apps explode on social media exactly one week before the payouts start. To stay ahead of them, you should always check the official SASSA Payment Dates page and plan your spending before the “easy credit” ads find you.

Millions of South Africans have been shut out of traditional banks for years. These digital lenders are filling that gap, but not in a good way. They don’t do real credit checks. You just need an ID and a bank account, and you’re approved in five minutes. A 2026 study by FinMark Trust found that 8 million people in our country are still underserved by big banks. These apps pretend to be a solution for “financial inclusion,” but they are really just extracting wealth from people who have the least.

The Debt Spiral: Real Stories from SASSA Recipients Trapped by Digital Loans

To understand how bad this is, you have to hear from the people living through it. I spoke to a few recipients who wanted to share their experiences.

Thembi’s Story: A 28-year-old mother in Tembisa used an app to buy school shoes for her son for R250. “It said three payments of R83. I thought I could manage,” she told me. She paid the first one, but then taxi fares went up and she missed the second debit by just R30. The app hit her with a R90 fee. Suddenly, she owed R173, which is nearly half her grant. Now she’s skipping meals to pay off the penalties.

Sizwe’s Story: A 34-year-old from Umlazi was looking for work and needed R100 for data. He used three different apps to juggle the costs. One app took a R30 “service fee” upfront, so he only got R70. To pay that back, he took a bigger loan from another app. Now he owes over R500 to three different companies. His R390 grant can’t even cover the debt. “I feel like I’m drowning,” he said. “The notifications never stop.”

Your 2026 Financial Defence Plan: How to Spot and Avoid the Digital Debt Trap

Protecting your R390 grant takes a lot of discipline. You have to build a wall around your money before the lenders get to it. Here is how I suggest you handle it:

- Use the 24-Hour Rule: If you see something you want to buy online, wait a full day. Usually, that “must-have” feeling disappears once the excitement wears off.

- Budget Before the Money Lands: Sit down with a pen and paper. List your food, electricity, and transport first. Whatever is left is what you actually have to spend. If there’s nothing left, you can’t afford the “easy payment.”

- Delete the Apps: If you find yourself browsing shopping apps when you’re bored, delete them. If the temptation isn’t on your home screen, you’re less likely to fall for it.

- Ask the Hard Questions: Before you click ‘buy’, ask: Do I really need this today? Can I save for it instead? What happens if I miss a payment? If a late fee is going to cost more than 10% of your grant, walk away.

- Go Back to Stokvels: I still believe community-based savings are the best way to handle emergencies. A trusted stokvel is safer, interest-free, and keeps the money within the community instead of sending it to a tech company’s bank account.

Frequently Asked Questions

What exactly is Buy Now, Pay Later (BNPL)?

Are all BNPL services and digital loans a scam?

What happens if I miss a BNPL payment for an item I bought?

Can these apps take money directly from my SASSA Gold Card or bank account?

How can I check if a digital lender is registered and legitimate?

Are there any safe alternatives to digital loans for a small emergency?

What is the biggest red flag to watch for with online loan apps in 2026?

Does using BNPL services in South Africa affect my credit score?

Read Next

SASSA June Payment Update: June 2026 Payment Cycle Confirmed

The June 2026 SASSA payment cycle is confirmed for 2, 3 and 4 June 2026 for the …

The R50 Billion Food Waste SHOCK: Why Your R390 SASSA Grant Can't Buy Food While SA Throws It Away

BREAKING May 2026: A shocking new report reveals South Africa wastes over R50 …

Comments & Discussions