Table of Contents

The South African Reserve Bank’s surprise interest rate hike in April 2026 might have bankers talking about inflation, but for millions of SASSA beneficiaries, it’s a punch to the gut. I’m tired of seeing the “mashonisa” industry thrive while the buying power of the R390 grant disappears. This hike is a gift to loan sharks and a trap for the vulnerable. This article looks at the link between this rate hike and the predatory lending industry, showing how it makes informal loans more expensive and locks people into a cycle of debt. You need to know their new tactics, the real cost to your grant, and how to protect your money.

{kind=link}

SARB’s Shock Move: What the April 2026 Rate Hike Really Means for Your Wallet

When the South African Reserve Bank (SARB) bumped interest rates by 50 basis points this week, it sent a ripple through the whole country. But let’s be honest: a 15-year high in the prime lending rate doesn’t just hurt people with home loans. It’s a direct threat to the R390 grant. It makes me angry that while banks get more expensive, the real danger is in the shadows.

Predatory lenders—the mashonisas—are already using this news as a flimsy excuse to hike their own illegal rates. The National Credit Regulator (NCR) saw a 35% jump in complaints late in 2025, and I expect that to hit 50% soon. People are desperate, and these sharks smell blood. They operate outside the law, using the official SARB announcement to justify prices that would never be allowed in a bank.

The Mashonisa’s New Playbook: How Loan Sharks Will Exploit the 2026 Rate Hike

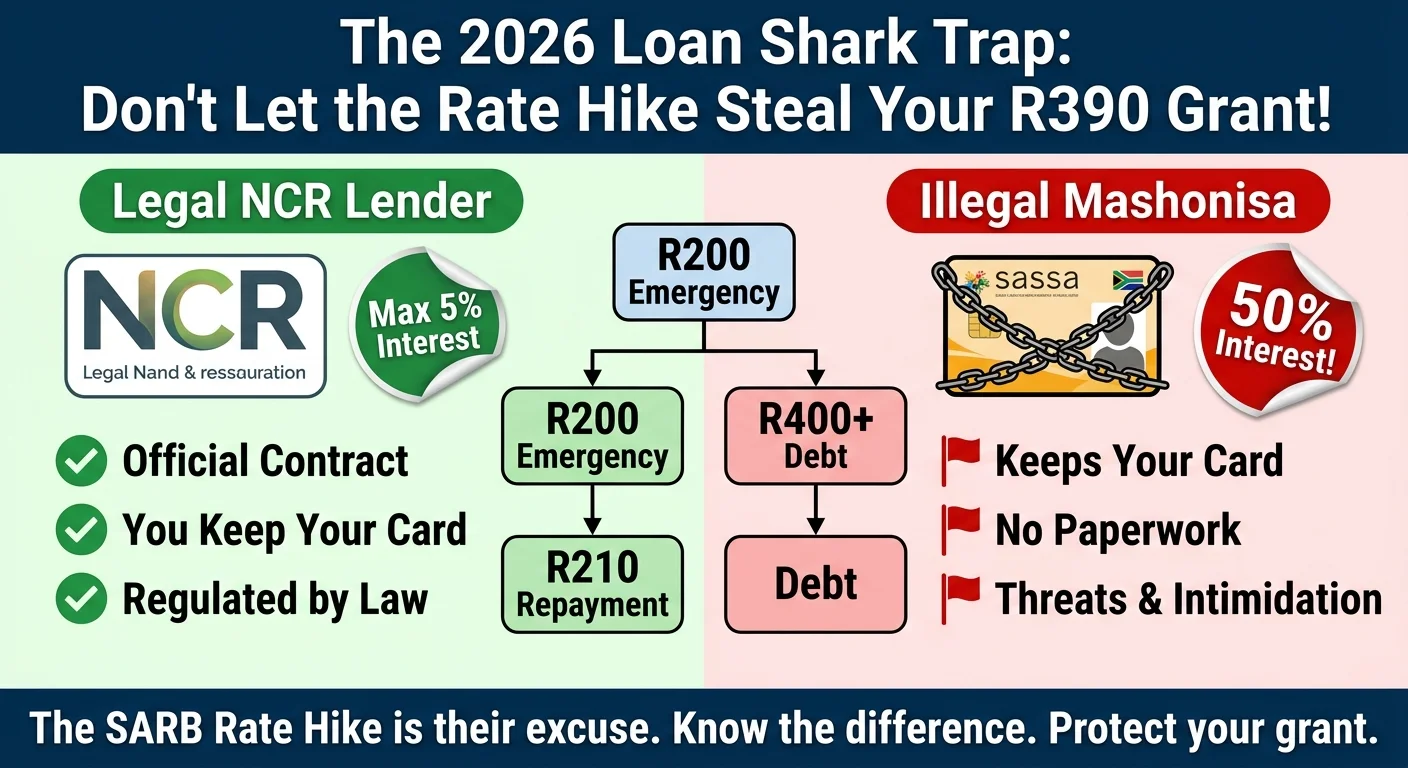

Loan sharks are opportunists, and the 2026 interest rate hike is their latest weapon. They’re getting bolder and, frankly, more manipulative. I expect they’ll start telling people their price hikes are “official” or “government-approved,” which is a flat-out lie.

Think about it: a R200 loan that used to cost R100 in interest might now cost you R150. That is a 75% interest rate for just a few weeks of “help.” It’s sickening. And they know you’re struggling, so the illegal practice of taking your SASSA card and ID book as collateral will likely get worse. Debt expert Nomvula Hlatshwayo says this isn’t about lending money; it’s about making sure you never get out of debt. It’s a trap that ensures beneficiaries can never fully pay back what they owe.

The R100+ Sting: Calculating the Real Cost to Your R390 Grant

Let’s look at the math, because it’s ugly. Before this April 2026 hike, borrowing R250 usually meant paying back R350. That R100 fee was already high. Now, a mashonisa will likely demand R400 for that same R250 loan. That’s R150 gone—nearly 40% of your entire R390 grant.

It leaves you trying to survive on R240 for the month. I hate calling this a “loan” because it’s really just a tax on being poor. If you do this for three months, you’ve paid R450 in interest just to borrow R250 once. It’s a spiral with no easy exit. If you’re feeling the squeeze, check the Payment Dates page to try and plan ahead, though I know how hard that is when the money is already gone.

Beyond Mashonisas: The Hidden Inflation on Food and Transport

The struggle doesn’t end with loan sharks. This rate hike hits the local spaza shop and the taxi rank too. Most informal traders buy their stock on credit. When their costs go up, your bread and maize meal prices go up.

A loaf of bread jumping from R20 to R22 might not seem like much to a banker, but it’s a big deal when every cent is accounted for. Taxi owners with vehicle loans will also feel the pressure, leading to higher fares. It feels like the R390 grant is being nibbled away from every direction. These small price increases are a form of hidden inflation that targets the people who can afford it least.

Your Defence Strategy: 5 Ways to Fight Back in 2026

It feels overwhelming, but you have more power than you think. Here is how I’d suggest fighting back in 2026:

- NEVER give up your SASSA Card or PIN. I cannot stress this enough. Giving your card away gives a stranger total control over your life. It’s illegal, so just say no.

- Understand the legal limits. A real, registered lender follows NCR rules. They can only charge 5% interest per month for short-term loans. If they want more, they’re a shark. Ask to see their NCR certificate.

- Look for community help. I know it’s hard to ask, but family or a stokvel is always better than a mashonisa. These groups are built on trust, not greed.

- You have rights. The National Credit Act is on your side. No one can legally threaten you or take your things without a court order.

- Report the sharks. Call the NCR at 0860 627 627. It’s scary to report someone in your neighborhood, but it’s the only way to stop the exploitation.

If your grant was declined and you’re thinking about a loan, please check our Appeals Guide first to see if you can get your funds sorted legally.

Frequently Asked Questions

What is an interest rate hike and why does it affect my R390 grant?

How can I tell if a loan shark is illegal in 2026?

Can a mashonisa legally keep my SASSA card or ID book?

What are the safe alternatives to loan sharks for a small emergency loan?

How much interest can a registered micro-lender legally charge in 2026?

Where can I report a predatory loan shark who is threatening me?

Read Next

SASSA June Payment Update: June 2026 Payment Cycle Confirmed

The June 2026 SASSA payment cycle is confirmed for 2, 3 and 4 June 2026 for the …

The R50 Billion Food Waste SHOCK: Why Your R390 SASSA Grant Can't Buy Food While SA Throws It Away

BREAKING May 2026: A shocking new report reveals South Africa wastes over R50 …

Comments & Discussions