Table of Contents

A comprehensive 2025 guide for South African SASSA beneficiaries on leveraging their R350 grant to access formal banking, secure affordable funeral cover, understand safe loan options, and use financial products to build stability. We break down the myths, expose the scams, and provide a step-by-step plan to turn your grant into a powerful financial tool.

{kind=link}

The R350 Grant Isn’t Just Survival Money—It’s Your Key to the Financial World

Let’s be honest. For millions in South Africa, the R350 SRD grant is a lifeline. It’s food, it’s transport, it’s a glimmer of hope in tough times. But what if we’ve been looking at it all wrong? What if that R350 is more than just cash for today? In 2025, the smartest beneficiaries are realizing a powerful truth: the R350 grant is a golden key. It’s the one piece of consistent income that can unlock the formal financial system—a system that often feels designed to keep the poor out. This isn’t another boring guide. This is the playbook on how to leverage your grant to get a bank account, protect your family with funeral cover, and even access safe credit, all while dodging the sharks that prey on the vulnerable.

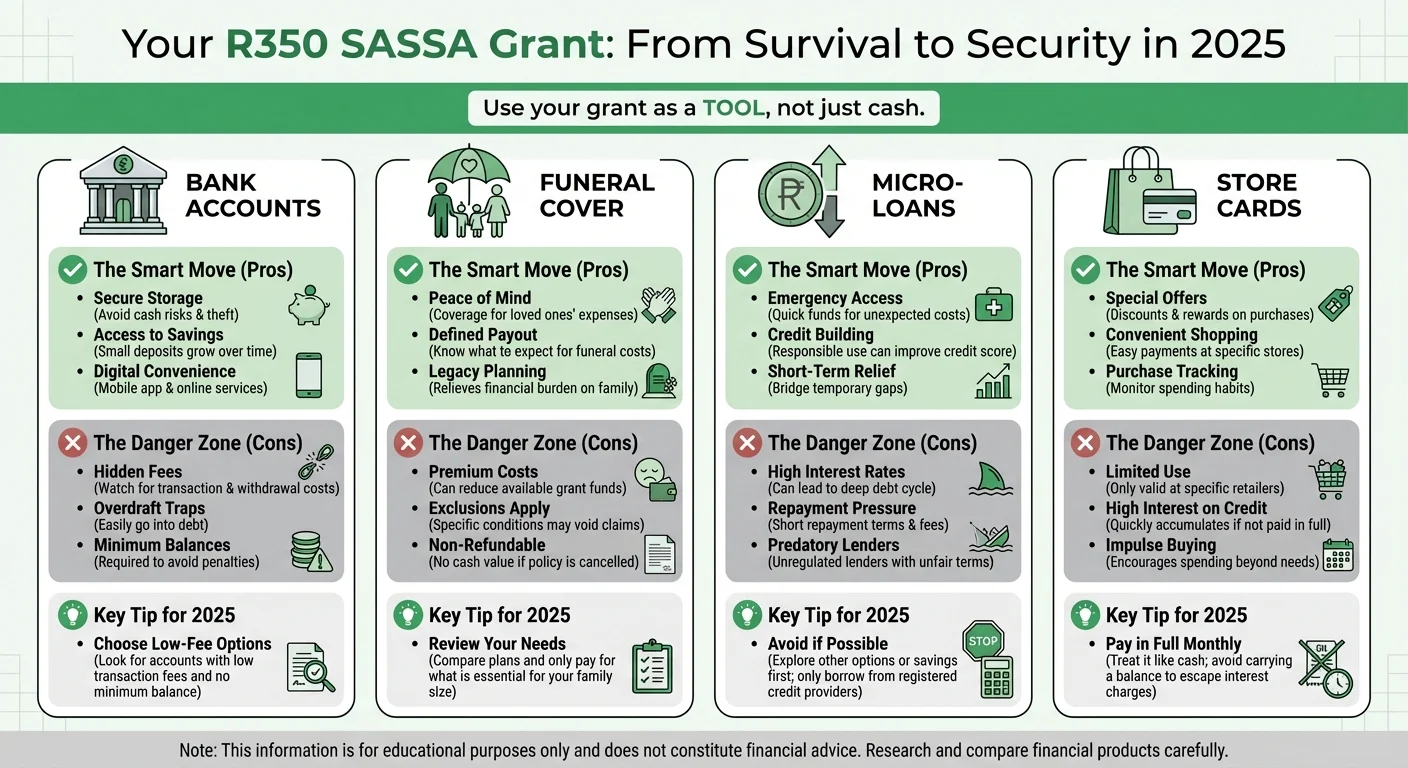

Power Move #1: Why a Bank Account is Your First Step to Freedom in 2025

Getting your grant paid into a bank account isn’t just about convenience; it’s a strategic move. The queues are a nightmare, and carrying cash is risky. But the real power lies in what a bank account represents: proof of financial activity.

Key Benefits for 2025:

- Safety: Your money is protected from theft or loss. Digital is safer than cash.

- Transaction History: This is your golden ticket. A history of monthly grant deposits is a form of ‘proof of income’ that can be used to apply for other services.

- Access to More Products: A bank account is the gateway to savings tools, affordable insurance, and other value-added services.

- Cost-Effective: With banks like TymeBank, Capitec, and the new digital offerings from Postbank, monthly fees can be as low as R5, which is often less than the transport money spent to collect cash.

Stop thinking of it as just a place to hold money. Think of it as your financial headquarters. To plan your budget around your grant, always check the official SASSA Payment Dates so you know exactly when your funds will arrive.

SASSA Myth Busters: Will a Bank Account Get My Grant Cancelled?

Let’s tackle the biggest fear head-on. Many people worry that if they open a bank account or have a small balance, SASSA will see it and cancel their grant. This is one of the most damaging myths out there.

The Truth for 2025:

- SASSA encourages banking: The agency actively wants beneficiaries to use bank accounts because it’s safer, more efficient, and reduces fraud.

- The Income Threshold Still Applies: SASSA’s main concern is the Means Test. As of 2025, you are disqualified if you have more than the specified income threshold flowing into your account from other sources (e.g., a salary). Your R350 grant deposit does NOT count as new income that disqualifies you.

- Small Savings Are Okay: Having a few hundred or even a couple of thousand Rand saved in your account from your grants will not automatically disqualify you. The system is looking for regular, incoming payments that indicate you have another source of income.

So, open that account with confidence. It’s a step towards empowerment, not a risk to your grant.

How to Open a Low-Cost Bank Account with Just Your SASSA Grant

Opening an account in 2025 is easier than ever. You don’t need a payslip or a formal job. Here’s what you generally need:

- Your Green Bar-Coded ID Book or Smart ID Card: This is non-negotiable.

- Proof of Residence: A utility bill, a letter from a councillor, or an affidavit from the police station. Some digital banks can verify your address online.

- Your Cellphone: You’ll need it for OTPs and banking apps.

Top Low-Cost Bank Choices for 2025:

- TymeBank: Kiosks in Pick n Pay and Boxer stores. No monthly fees for many transactions.

- Capitec: Low monthly fees and a great mobile app. Easy to open an account in-branch.

- Postbank: With its move towards a full-service bank, Postbank aims to be a primary choice for grant recipients. Keep an eye on their new offerings.

Once your account is open, you can easily update your payment details on the SASSA portal. Ensure your grant is approved by doing a quick SRD R350 Status Check before submitting your new banking details.

The Funeral Cover Dilemma: Protecting Your Family Without Getting Scammed

In our communities, a dignified burial is a final act of love and respect. But predatory funeral policies often target grant recipients with high premiums and clauses that make it impossible to claim. Your R350 grant makes you eligible for legitimate, affordable cover.

What to Look For in 2025:

- Low Premiums: You can find reputable cover for as little as R40-R80 per month for an individual.

- Registered Underwriter: Make sure the policy is backed by a major, registered insurance company (e.g., Sanlam, Old Mutual, Hollard).

- Clear Waiting Periods: Understand the waiting period for natural death (usually 6 months) and accidental death (usually immediate cover).

- No-Lapse Benefits: Some policies have a grace period if you miss a payment, which is crucial when grant payment dates sometimes shift.

Red Flags to Avoid:

- Pressure to sign up immediately.

- Unclear terms and conditions.

- Policies that are not underwritten by a registered Financial Service Provider.

Your grant is a tool to provide peace of mind for your family, not to enrich a scammer.

Navigating Loans: The Dangerous Line Between ‘Mashonisas’ and Safe Credit

When an emergency strikes, a loan can feel like the only option. This is where grant recipients are most vulnerable. Loan sharks (‘mashonisas’) who hold your ID and SASSA card are illegal and dangerous. But your grant can be used to access small, safe, and regulated loans.

The Difference Between Good Debt and Bad Debt:

- Bad Debt: High-interest loans from unregistered lenders that trap you in a cycle of repayment you can never escape. They often illegally take your SASSA card as collateral.

- Good Debt (Micro-loans): Small loans from registered credit providers (like those offered by banks or reputable microlenders) with clear repayment terms and regulated interest rates. These are meant to be paid off quickly.

Before you even consider a loan, ask yourself: Is this an absolute emergency? Can I comfortably afford the repayments from my grant? A R500 loan can quickly balloon into thousands with the wrong lender. Never borrow money for non-essentials. If your grant application was unfairly declined and you’re in a tough spot, rather focus your energy on the official SASSA Appeals Guide to get your income reinstated.

Store Cards vs. Bank Accounts: The 2025 Showdown

Many retail stores like Pep, Ackermans, and Jet offer store accounts to SASSA beneficiaries. They can be tempting for buying clothes or school supplies on credit. Let’s break down the pros and cons.

Store Cards:

- Pros: Easy to qualify for, allows you to buy essential goods on credit, can help build a credit history.

- Cons: High interest rates (often over 20%), can only be used at that specific store, encourages over-spending, and can quickly lead to debt if not managed carefully.

Bank Account (Debit Card):

- Pros: You spend money you actually have (no interest), can be used anywhere, encourages budgeting and saving.

- Cons: You can’t spend more than you have, which can be difficult in an emergency.

Our Verdict: A bank account is always the safer, primary option. Use it for your daily needs. Only consider a store card for a specific, planned purchase you know you can pay off within a month or two. Never max it out.

Building a Credit History on R350 a Month? Yes, It’s Possible.

A credit history is a record of how you manage debt. Having no credit history can be as bad as having a poor one. By using your R350 grant smartly, you can slowly build a positive record.

How to Do It in 2025:

- Open a Bank Account: This is the first step. It shows financial stability.

- Get a Small, Manageable Account: A clothing account (like from Mr Price or TFG) that you use for one small purchase (e.g., R100) and pay off immediately and in full at the end of the month.

- Consider a Cellphone Contract: A small, entry-level cellphone contract that you pay on time every month via debit order from your grant-funded bank account is a powerful way to build credit.

Consistency is key. Small, consistent, on-time payments show credit providers that you are a responsible client, opening doors for you in the future.

Warning Signs: How to Spot a Financial Scam Targeting You in 2025

Scammers are creative and ruthless. They know grant recipients are often in desperate situations. Here are the red flags to watch for:

- “We work with SASSA”: SASSA does not partner with any credit providers for loans. This is a lie.

- Upfront Fees: You should never have to pay a fee to get a loan or insurance policy.

- Requests for your PIN: Never share your card PIN with anyone for any reason.

- Blank Documents: Never sign a blank contract or document.

- WhatsApp Loans: Legitimate lenders have formal application processes, not just a WhatsApp number.

- Guaranteed Approval: No legitimate lender can guarantee approval before checking your details.

If it sounds too good to be true, it always is. Protect your grant and your identity. If you haven’t started receiving your grant yet, make sure you follow the official process outlined in our Complete SRD Grant Application Guide.

Your 2025 SASSA Financial Action Plan

Feeling empowered? Here’s a simple checklist to get you started on turning your R350 grant into a powerful financial tool:

- This Month: If you’re still collecting cash, make a plan to visit a bank (like Capitec or a TymeBank kiosk) to open a low-fee account. Get the required documents ready.

- Next Month: Once your grant is paid into your new account, find one reputable company for funeral cover. Get a quote for a premium you can comfortably afford (e.g., under R60).

- The Next 3-6 Months: Focus on consistency. Let your grant be paid into your account every month. Do not take on any debt. Get used to using a debit card and budgeting.

- Long-Term Goal: Once you have a stable routine, consider one small, manageable credit item (like a clothing account) to start building a positive credit history. Pay it off in full every single month.

This patient, strategic approach will put you miles ahead and build a foundation for real financial security.

Frequently Asked Questions

Can I get a loan if I only receive a SASSA R350 grant in 2025?

What is the cheapest bank account for SASSA beneficiaries in South Africa for 2025?

Does having funeral cover affect my SASSA grant application?

Will taking a loan affect my R350 grant eligibility?

How can I prove my income to a bank with only a SASSA grant?

Are store accounts from Pep or Ackermans a good idea for grant recipients?

What happens to my funeral policy if my grant stops?

Can I use my SASSA card to apply for loans or insurance online?

Read Next

SASSA's New 'Mandatory App' Locks Your R390 Grant? The 2026 Guide for Beneficiaries Without a Smartphone

BREAKING April 2026: SASSA is rolling out a mandatory new smartphone app, …

The R140 Paraffin Price SHOCK: How 40% of Your R390 SASSA Grant Will Vanish on May 1st, 2026

BREAKING April 2026: NERSA has approved a devastating 40% increase in the price …

Comments & Discussions