Table of Contents

In January 2026, millions of South Africans depend on their SASSA grants. But a shadow industry of banks, insurers, and lenders sees this as an opportunity. This article uncovers the common financial traps—from hidden bank charges to high-interest store cards and predatory loans—that can leave you with nothing. Learn to identify these schemes, understand your rights, and take control of your money with our expert guide for 2026.

{kind=link}

The Hidden War on Your R350: A January 2026 Reality Check

For millions in South Africa, the SASSA R350 Social Relief of Distress (SRD) grant is not just money; it’s a lifeline. It’s food on the table, transport for a job interview, or data to connect with family. Yet, as we enter January 2026, a fierce, often invisible battle is being waged for every single Rand of that grant. It’s a war fought not with weapons, but with debit orders, complex contracts, and persuasive sales tactics. This isn’t just about managing money; it’s about defending it from a system that is increasingly designed to chip away at the financial support meant for the most vulnerable. This investigation pulls back the curtain on the financial traps that specifically target SASSA beneficiaries and shows you how to fight back.

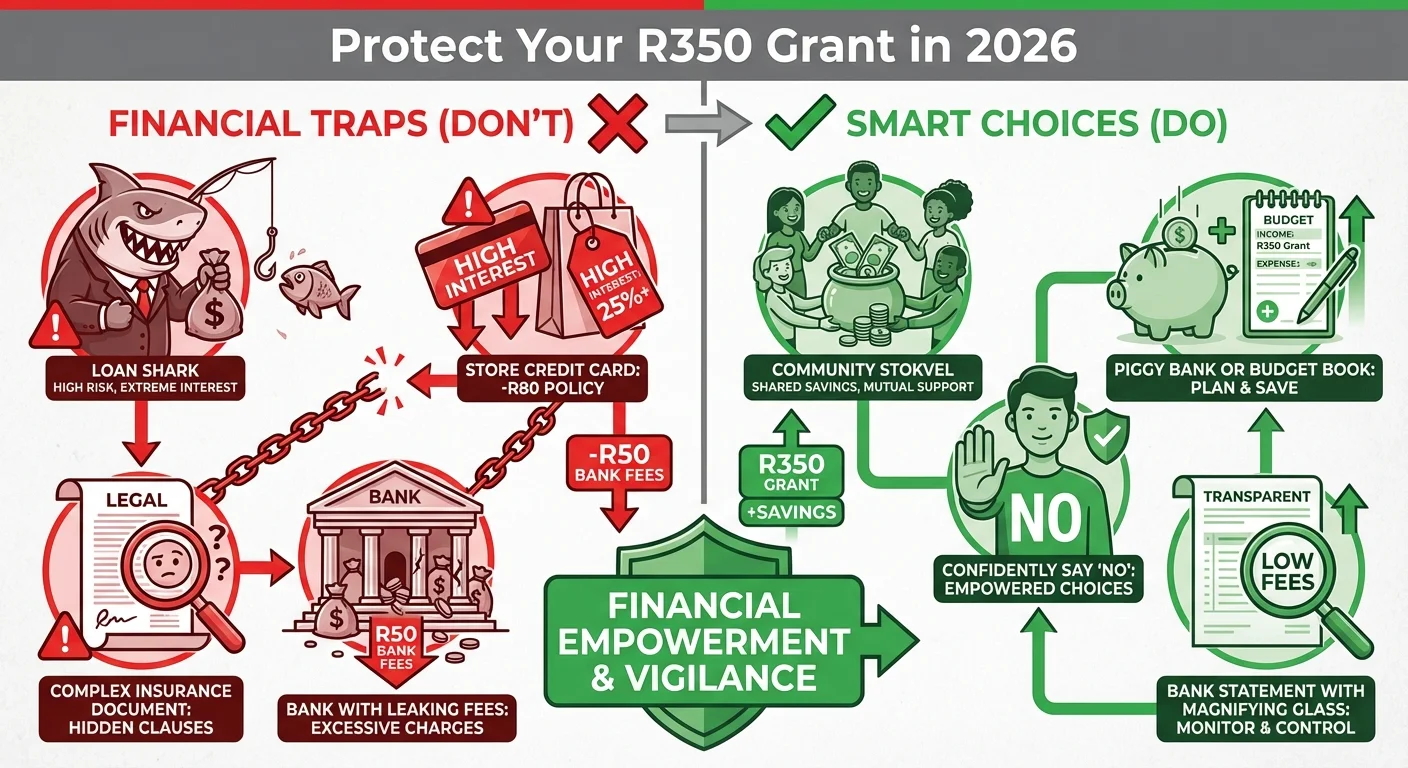

Trap 1: The ‘Low-Cost’ Bank Account That Costs You a Fortune

The government’s push for beneficiaries to move from Postbank to commercial bank accounts was meant to improve efficiency. The reality in 2026? A minefield of hidden fees. Banks advertise ’low-cost’ or ‘pay-as-you-transact’ accounts, but for a grant recipient, these costs are devastating. A R5 withdrawal fee here, a R10 monthly admin fee there, a R2 fee for a balance inquiry—it adds up. By the end of the month, up to 15% of your R350 grant can be consumed by bank charges alone. This is the first line of attack on your grant. Before you even spend it, the bank has taken its share. It’s crucial to scrutinize these fees and demand transparency. Knowing when your funds will arrive by checking the official SASSA Payment Dates can help you plan withdrawals to minimize these costs.

Trap 2: The Aggressive Push for Funeral Cover You Can’t Afford

In South African culture, a dignified burial is paramount. Insurers know this and exploit it mercilessly. SASSA pay points and community centres are hunting grounds for agents selling funeral policies. They promise peace of mind but deliver a contract that siphons R80-R150 a month from your grant. The pressure is immense, the language confusing. Many beneficiaries sign up without fully understanding the terms, only to find their policy lapses if they miss a single payment, losing everything they’ve contributed. This isn’t insurance; it’s a gamble where the house almost always wins. In 2026, we are seeing an increase in digital-only policies with even less transparency, making it harder to question deductions.

Trap 3: The Store Card Debt Spiral

Major retailers have become adept at targeting SASSA beneficiaries. They offer store cards with enticingly low initial credit limits—R250 or R500. It seems harmless; a way to buy groceries before your grant arrives. But with interest rates often exceeding 25% per annum, that R300 purchase of maize meal and cooking oil quickly balloons into a R500 debt. The minimum payments are designed to keep you in debt for as long as possible. Suddenly, your grant arrives, and a significant portion is immediately swallowed by a debit order for a store card, forcing you to rely on the card again. It’s a vicious cycle designed to create dependency.

Trap 4: ‘Easy Money’ from Microlenders and Mashonisas

When unexpected expenses arise, the temptation of an ’easy loan’ is strong. Registered microlenders and unregistered loan sharks (mashonisas) are always ready to offer cash, often demanding your SASSA card and PIN as collateral—an illegal practice. The interest rates are astronomical, sometimes 50% per month. A R200 loan can become a R600 debt in a few months. These lenders are ruthless, and their collection methods can be intimidating. This is the most dangerous trap, turning a temporary cash flow problem into a long-term financial nightmare. Ensuring your grant is approved by doing a regular SRD R350 Status Check is vital to avoid the desperation that leads to these loans.

The Silent Thieves: Airtime and ‘Value-Added’ Service Deductions

Perhaps the most infuriating deductions are the small, unexplained ones for airtime, data, or ‘digital content’ services you never subscribed to. These often stem from clicking a link or responding to a promotional SMS. While individually small (R5, R10, R20), these ‘ghost’ deductions can amount to a significant loss over a year. They prey on the fact that many people won’t go through the hassle of disputing such a small amount. In 2026, these automated scams are more sophisticated than ever, making it crucial to guard your phone number as closely as your bank details.

SASSA’s Stance: What You Can Officially Do

SASSA has consistently stated that it is against any unauthorized deductions from social grants. They have a formal process for disputes. If you see a deduction you don’t recognize, you have the right to challenge it. You can fill out a form at a SASSA office or contact their helpline. However, the process can be slow and frustrating. The most effective first step is often to deal directly with your bank to place a stop order on the debit. For illegal lenders who have taken your card, you should report it to the police and SASSA immediately. If your grant application details are incorrect, it can cause payment delays, which might push you towards these traps; it’s always wise to follow the Complete SRD Grant Application Guide to ensure everything is in order.

Your 2026 Battle Plan: How to Protect Your Grant

Knowledge is your shield. Here is your action plan to defend your money:

- Become a Detective: Get a printed bank statement every month. Read every single line. Question every deduction, no matter how small. Use banking apps to monitor your account in real-time.

- Learn to Say NO: Salespeople are trained to be persuasive. Your most powerful word is ‘No’. Say, ‘I need to think about it,’ ‘Let me read the contract at home,’ or simply, ‘No, thank you.’ Do not be pressured into signing anything on the spot.

- Use the Official Dispute Channels: For unauthorized debit orders, immediately contact your bank to reverse it and block the company. For suspected fraud, use SASSA’s dedicated fraud hotline.

- Choose the Right Bank Account: Research is key. Look for accounts with zero monthly fees, free withdrawals at specific ATMs, and no charge for electronic payments. Compare options from TymeBank, Capitec, and other providers to find the best fit for your needs.

- Never, Ever Share Your PIN or Card: Your SASSA card and PIN are yours alone. Giving them to anyone is not only dangerous but illegal. No legitimate lender will ask for them.

Smarter Alternatives to Debt

Escaping these traps requires finding better alternatives. Instead of turning to lenders or store credit, consider these options:

- Stokvels and Community Savings: For centuries, South Africans have used stokvels to save and support one another. Joining a trusted, local stokvel can provide a safety net for emergencies and a way to save for larger purchases without incurring interest.

- Budgeting: It sounds simple, but actively planning where every Rand of your R350 will go is a game-changer. Prioritize needs (food, transport) over wants. There are many free budgeting apps available or you can use a simple notebook.

- Community Support: Lean on family, trusted friends, or community organizations like churches when you are in a tight spot. A small, interest-free loan from a relative is infinitely better than a mashonisa. If your grant has been unfairly declined, lodging an appeal is a crucial step to restore your income; follow our comprehensive Appeals Guide for help.

Conclusion: Your Grant, Your Power

The R350 grant is a recognition of your dignity and your right to social support. It is not a revenue stream for predatory companies. In January 2026, the responsibility falls on you to be vigilant, to question everything, and to protect your lifeline. By understanding these traps and embracing smarter financial habits, you reclaim power over your money. You transform from a target into a savvy consumer who makes every Rand work for you, not for them.

Frequently Asked Questions

Can SASSA stop deductions from my bank account in 2026?

Which bank is the best and cheapest for a SASSA grant?

Is it illegal for a lender to take my SASSA card and PIN?

I signed up for a funeral policy I don't want. How can I cancel it?

What happens if I can't pay my store card account?

How can I check for unauthorized subscriptions on my phone?

*135*997#. For MTN, it’s *141*5#. These services allow you to view and cancel active subscriptions that deduct airtime.Are all microlenders bad?

Where can I get free financial advice in South Africa?

Read Next

SASSA's New 'Mandatory App' Locks Your R390 Grant? The 2026 Guide for Beneficiaries Without a Smartphone

BREAKING April 2026: SASSA is rolling out a mandatory new smartphone app, …

The R140 Paraffin Price SHOCK: How 40% of Your R390 SASSA Grant Will Vanish on May 1st, 2026

BREAKING April 2026: NERSA has approved a devastating 40% increase in the price …

Comments & Discussions