Table of Contents

Title: The R99/Month Funeral Policy SCAM: How Your R390 SASSA Grant is Stolen Legally in 2026

With millions of South Africans relying on the R390 SRD grant to put food on the table, predatory companies are aggressively marketing R99/month funeral policies that offer almost no value. This SASSA-targeted trap is designed to look like a bargain, but it’s a high-risk gamble with your survival money.

{kind=link}

The New Financial Predator: How R99 Policies Target 8 Million SASSA Beneficiaries

A report from the Financial Sector Conduct Authority (FSCA) in May 2026 has confirmed what many of us already feared. There is a massive crisis targeting South Africa’s most vulnerable people, and it involves the aggressive selling of predatory funeral policies to SASSA grant recipients. With over 8.5 million people now surviving on the R390 Social Relief of Distress (SRD) grant, insurers are sending high-pressure sales teams into our communities. They promise a “dignified death” for just R99 a month.

I want to be clear: this isn’t about helping people. It is a cold, calculated business model. That R99 price point is chosen specifically because it sounds affordable, but it actually eats up a staggering 25% of a beneficiary’s monthly income. I find it deeply concerning that the fear of a pauper’s burial is being used to trick people into signing contracts they don’t understand. The FSCA shows that 1 in 5 SRD grant recipients now has a funeral policy debit order, and many of these are with unregistered or unethical providers. This isn’t just a bad deal, it’s a national emergency that is siphoning social relief funds straight into the pockets of predators.

Deconstructing the Deception: “Guaranteed Payout” and Other Lies You’re Being Sold

The sales pitch for these policies is designed to play on your emotions. Agents use high-pressure tactics and exploit our cultural respect for funeral rites. The biggest lie they tell is the promise of “guaranteed acceptance.” While they might let anyone sign up, they make it nearly impossible to actually claim the money later.

The policy documents are usually buried under complex clauses that most people never see. For example, many of these policies have a 6-to-12-month waiting period for a natural death. If your loved one passes away from an illness during that time, the company pays nothing, or they might just refund the premiums you paid. They also love to promise “instant payouts,” but the reality is a nightmare of paperwork and delays. According to the Long-Term Insurance Ombudsman’s 2025 report, over 30% of complaints were about denied funeral claims. Sales agents will never mention these risks because they only care about getting your signature and banking details to secure their own commission.

The R390 Drain: Calculating the True Annual Cost of a Predatory Policy

That “small” R99 premium is the bait, but the long-term drain on your R390 grant is the real trap. Let’s look at the actual numbers. A R99 monthly policy costs you R1,188 every year. If you are living on the SRD grant, that is more than three full months of your income gone. That is money that should be going toward food, electricity, or transport.

Now, look at the payout. A typical predatory policy might offer a R10,000 benefit. After paying R1,188 every year, you would have to pay in for over 8 years just to match what they eventually pay out. These companies actually count on you missing a payment. If you miss just one debit order, the policy can lapse immediately. All the money you’ve paid—hundreds or thousands of Rands—is gone forever. You lose everything. These companies keep a close eye on the SASSA grant schedule, which you can find on our Payment Dates page, and they time their debit orders to hit your account the second your grant arrives.

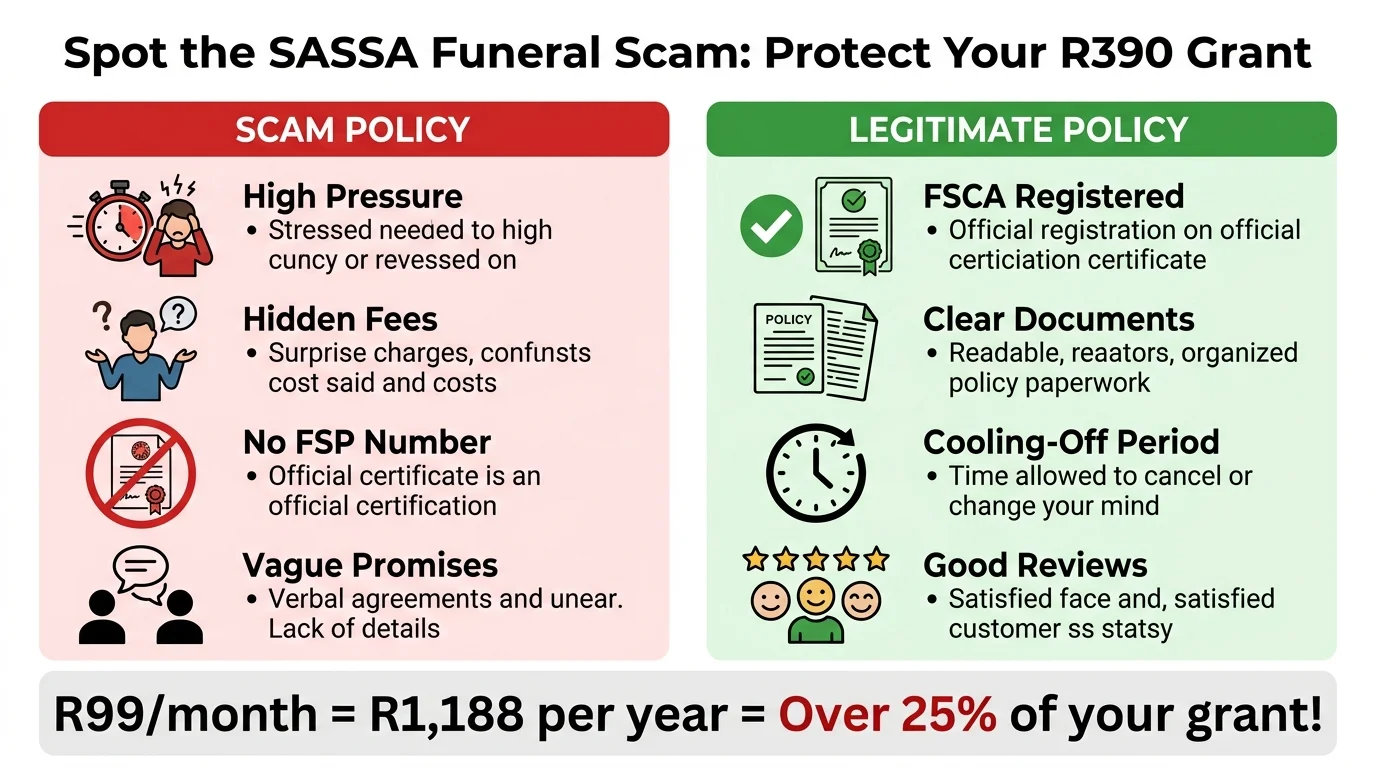

RED FLAG CHECKLIST: How to Spot a Funeral Scam Before You Sign

You have to be vigilant to protect your grant. Before you sign anything or give away your bank details, use this list to spot a scam. If you see any of these signs, walk away immediately.

- Extreme Pressure: If they say you must sign “right now” or the offer will vanish, they are trying to stop you from thinking clearly.

- No FSP Number: Always ask for their Financial Services Provider (FSP) number. If they can’t show it, or if it doesn’t work on the FSCA website, they are illegal.

- Vague Paperwork: If they only show you a pretty brochure and won’t give you the full document with all the “fine print,” don’t sign.

- Asking for your PIN: This is a huge red flag. A real company will never, ever ask for your SASSA card PIN.

- Cash Demands: If an agent wants the first premium in cash, they are likely just stealing it. Legitimate payments happen through official bank channels.

- Hidden Underwriters: If “XYZ Funerals” is selling the policy, ask who is actually backing it. A real policy is always backed by a major, registered insurer like Sanlam or Old Mutual.

Safer Alternatives: Legitimate Funeral Cover on a SASSA Budget

You can still get a dignified funeral without falling into a trap. There are better ways to handle this, even on a tight budget. First, stick with well-known insurance companies that have been around for years. Many offer basic, low-cost policies for R30 to R50 a month. These are properly regulated by the FSCA.

Another option is joining a Burial Society (Stokvel). These are community groups where people actually know and care about each other. They are often much more flexible than a big corporation. Members contribute a small amount each month, and the money helps the family when someone passes away. The National Stokvel Association of South Africa (NASASA) notes that these societies are a vital safety net for our people. Some banks also offer basic cover as a cheap add-on to your account. Whatever you choose, do your homework and verify the FSP number on the FSCA website.

Your Rights: How to Cancel a Bad Policy and Report Fraudsters in 2026

If you’ve already been talked into a bad policy, don’t panic. You have rights, and the law is there to protect you. Under the Policyholder Protection Rules, you have a “cooling-off” period. This means you have 31 days from the day you get your policy documents to cancel it for any reason and get a full refund of your money.

To do this, you should contact the insurance company in writing—an email is best so you have proof. If you are past the 31 days, you can still cancel, though you probably won’t get your old premiums back. You should also report the company if they lied to you. File a complaint with the Financial Sector Conduct Authority (FSCA). They are the ones who can fine or shut down these predators. If a legitimate company is refusing to pay a claim, contact the Ombudsman for Long-Term Insurance. Their service is free and they help resolve disputes fairly. Taking a stand doesn’t just help you, it protects your whole community from these traps.

Frequently Asked Questions

Can a funeral policy company legally debit my SASSA grant account?

Is R99 a month too much for funeral cover on an R390 grant?

How can I verify if a funeral policy provider is legitimate in South Africa in 2026?

What happens if I miss a payment on my funeral policy because my SASSA grant is late?

Are burial societies safer than formal funeral policies for SASSA beneficiaries?

What is the FSCA and how can it help me?

Can I have more than one funeral policy?

What is a policy 'underwriter' and why is it important?

Read Next

SASSA June Payment Update: June 2026 Payment Cycle Confirmed

The June 2026 SASSA payment cycle is confirmed for 2, 3 and 4 June 2026 for the …

The R50 Billion Food Waste SHOCK: Why Your R390 SASSA Grant Can't Buy Food While SA Throws It Away

BREAKING May 2026: A shocking new report reveals South Africa wastes over R50 …

Comments & Discussions