Table of Contents

Title: Your R390 March Grant is Already Gone: How New 2026 Bank Fees Will Eat R40 of Your SASSA Payment

If you were counting on the extra cash from the SASSA R390 grant this March, I have some bad news. While the government talked up the R20 increase, the banks were quietly sharpening their knives. By the time you actually get your hands on that money, those new 2026 bank fees will have already taken a massive bite out of it.

{kind=link}

The R20 Illusion: Your March 2026 Grant Increase is a Mirage

The R20 increase to the SRD grant, which pushed it to R390, was framed during the February 2026 Budget Speech as a win for the poor. For the 8.8 million South Africans who rely on this money to survive, every cent counts. But I’ve been looking at the numbers, and this “increase” feels like a cruel joke. It’s being swallowed whole by annual bank fee hikes.

As you get ready to collect your March 2026 payment, you’re essentially walking into a trap. Big names like Capitec, FNB, Standard Bank, and Absa have all updated their fee schedules to hit right on March 1st. The very first time you try to access your R390, you’ll likely pay more in fees than you did last month. You can check the latest official payout schedule on our Payment Dates page, but the reality remains the same. The financial sector is effectively clawing back the state’s help, leaving the most vulnerable people in South Africa right back where they started.

The Hidden Tax: Unpacking the 2026 Bank Fee Hikes

These 2026 bank fees are basically a “hidden tax” on the poor. If you’re wealthy, a few extra rand in fees is annoying. If you’re living on R390 a month, it’s a disaster. The banks are specifically targeting cash transactions, which is exactly how most SASSA beneficiaries use their money.

Here is what the new fee structures actually look like:

- ATM Cash Withdrawal Fees: This is where they really get you. Withdrawing from an ATM that doesn’t belong to your bank could now cost you R15 plus a percentage of the cash. Even using your own bank’s ATM has climbed to around R10 or R12.

- Decline Fees: This is the most offensive fee of all. If you try to draw money and don’t have enough because you forgot to account for the fee itself, the bank charges you anyway. You lose R7 to R9 just for being broke.

- Over-the-Counter Fees: Don’t even think about going inside a branch. Fees there are now over R50, which forces everyone toward ATMs and retailers.

- Balance Enquiry Fees: Checking your balance at an ATM can now cost R5. Do that a few times and you’ve already lost a loaf of bread.

The Banking Association of South Africa’s 2025 reports show that transaction volumes are higher than ever. The banks are making a killing while the people at the bottom pay the highest price for basic access to their own funds.

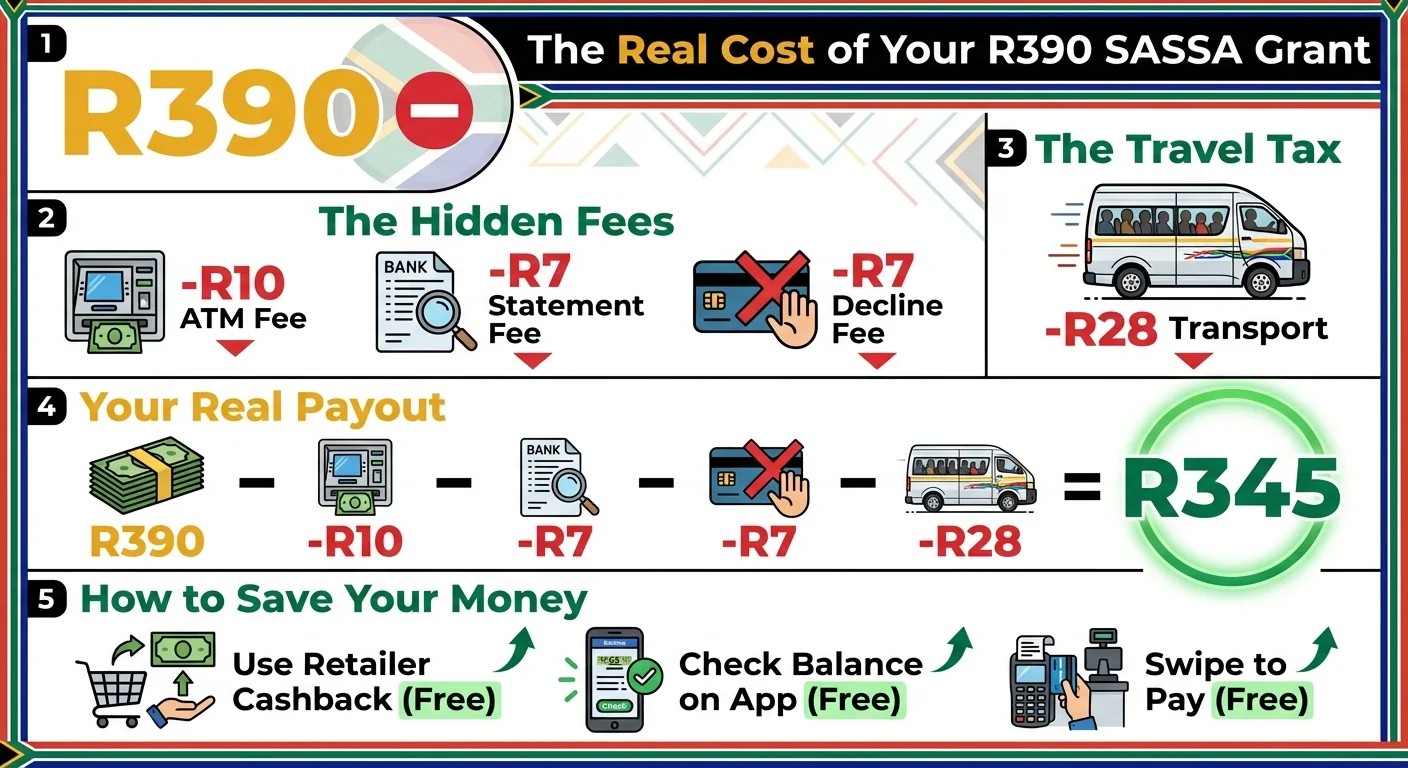

From R390 to R350: A Real-World Cost Breakdown

Let’s look at what this actually looks like for a real person in March 2026. The government says you get R390, but your wallet says something different.

- Transport Cost: You have to get to the ATM or the shop. A taxi there and back is going to cost you about R28.

- ATM Withdrawal Fee: You use your bank’s ATM. That’s another R10 gone.

- The Unexpected Decline: You try to draw R380, but the R10 fee makes the total R390. Sometimes the system glitches or you miscalculate. Boom—a R7 decline fee.

- Successful Withdrawal: You finally get R370 out.

The math is depressing:

- Starting Grant: R390

- Minus Transport: -R28

- Minus Decline Fee: -R7

- Minus Withdrawal Fee: -R10

Total Cost of Collection: R45

Your actual take-home cash is R345. That R20 increase didn’t just disappear; it took another R25 of your original grant with it. You’ve lost over 11% of your money just trying to touch it. And this doesn’t even count the airtime you spent checking your status or the risk of the ATM being offline in rural areas, which happens way more often than the banks like to admit.

Your 5-Step Plan to Reclaim Your R40 This March

I hate seeing this money go to waste, but you can fight back. You have to change how you collect your money if you want to keep that R40. Here is how you handle the March 2026 cycle:

Use Retailer Cashback (Your Best Move): Stop using ATMs. Go to Shoprite, Checkers, Pick n Pay, or Boxer. Buy something small that you actually need—like a R20 loaf of bread—and ask for the rest of your grant as cashback. The withdrawal is free, and you save that R10 ATM fee immediately.

Tap-to-Pay for Everything: You don’t need to carry all that cash. Use your SASSA card at the till. Swiping or tapping is free. It keeps your money safe and saves you a trip to the ATM.

Check Your Balance for FREE: Do not pay R5 to an ATM. Use the SRD Status Check portal on your phone first. Then, use your bank’s free USSD code (like Capitec’s

*120*3279#) or their app while you’re on Wi-Fi.The One-Withdrawal Rule: If you absolutely must have cash from an ATM, take it all out at once. Every time you put that card in the machine, the bank takes another R10. Plan your budget so you only pay that fee once.

Look Into Zero-Fee Accounts: Switching banks is a mission, but accounts like TymeBank or Bank Zero are much cheaper. Since they work with Pick n Pay and Boxer, they are often a much better fit for anyone on a SASSA grant.

A Call to Action: It’s Time for a Social Grant Banking Standard

The way bank fees eat into social grants is a massive policy failure. It makes no sense for the state to hand out R390 only for private banks to take 10% of it for doing almost nothing. This isn’t just a banking issue; it’s a social justice issue.

Social policy expert Dr. Zama Khumalo says it best: “The value of a social grant must be measured by its purchasing power, not its face value.” If it costs R40 to get your money, the grant isn’t R390—it’s R350.

I believe the Department of Social Development and the National Treasury need to stop playing nice and force banks to offer a “Social Grant Account.” This should include at least one free withdrawal, free swipes, and free digital balance checks. Until that happens, the banking sector is essentially getting a government-funded handout at the expense of South Africa’s most vulnerable citizens.

Frequently Asked Questions

What are the new bank charges for SASSA grants in 2026?

How can I avoid paying ATM fees on my R390 SASSA grant?

Is it completely free to get SASSA cashback at Shoprite?

Why did my bank charge me for a failed SASSA withdrawal?

What is the cheapest bank for SASSA beneficiaries in 2026?

How much does it cost to check my SASSA balance at an ATM in 2026?

Read Next

SASSA May 2026 'Double Holiday' Payout WARNING: Why Your R390 Grant Could Be Delayed

BREAKING April 2026: The back-to-back Freedom Day (27 April) and Workers’ …

The R99 Funeral Cover 'Scam' Siphoning 25% of Your R390 SASSA Grant in 2026

BREAKING for April 2026: A wave of aggressive R99-per-month funeral policies is …

Comments & Discussions